ru 486 abortion pill where to buy

how to buy abortion pill

adamzastawski.com abortion pill buy

fjrigjwwe9r3SDArtiMast:ArtiCont

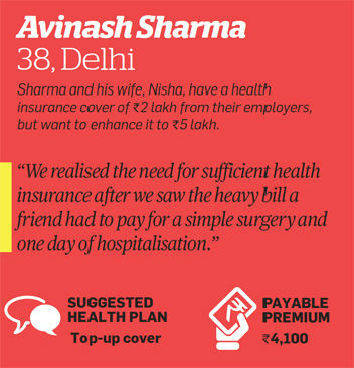

It takes an agent several days, even weeks, to convince a customer to buy health insurance. Yet, 10 minutes at the billing counter of a hospital were enough to persuade Avinash Sharma.

When the Delhi-based professional visited a friend, who had undergone a minor surgery in a private hospital last month, he was shocked to see the bill at the time of discharge. "A simple operation and one night�s hospitalisation cost him Rs 1.4 lakh. The cover from his employer covered only Rs 50,000 of the cost," he says. We are not surprised. Healthcare costs are rising at a fast clip. According to a survey by insurance consultancy firm, Towers Watson India, healthcare costs in India increased by 13.25% in 2011.

Case of Avinash Sharma

The rate of increase in 2012 is estimated to be roughly at the same level. The culprits: introduction of new medical technologies, over-prescription by doctors, and a general rise in medicine costs. Says Antony Jacob, CEO of Apollo Munich Health Insurance: "The treatment protocol for angioplasty today is vastly different from that followed five years ago. Many of these advanced medical technologies and procedures cost more." Sharma is now looking for a health insurance policy for his family. However, the vast array of choices before him is confusing. There are individual policies and family floater plans, policies that restore the limit after the claim and plans that cover critical illnesses or offer cash benefits on hospitalisation. How does one pick a suitable plan from this clutter? The answer is that your needs should define the type of policy you buy. Each type of health insurance policy fulfils a certain need (see graphic). The choice depends on the buyer�s age, family size and structure, and existing insurance cover.

|

|

|

Young nuclear family

If you have a nuclear family, a family floater plan will suit you best. In these plans, the cover is shared by the entire family. The premium per Rs 1 lakh may be higher compared with an individual policy, but the premium per person works out to be lower. It�s a calculated risk you can safely take. It is unlikely that all the members will require hospitalisation in the same year. For newly married couples, who intend to start a family in a few years, it makes sense to plan accordingly. Though most health insurance policies do not cover maternity costs, some do. However, these costs are covered only after a waiting period of 2-3 years. Buy a policy that covers maternity costs immediately after marriage.

Covered by employer

Some people believe that if they are covered by their employer, they don�t need to buy a separate policy. This can be a costly mistake. While such covers are useful, they may not be sufficient. If you lose your job or switch to another company, you may be rendered uninsured. Even if you buy a fresh cover immediately, keep in mind that there is a mandatory 45-day cooling period during which certain claims will not be paid.

Before you switch to a new insurer

Besides, there is a 2-3 year waiting period for pre-existing diseases. This is where the employer-provided cover is very handy, points out Roopam Asthana, CEO and wholetime director at Liberty Videocon General Insurance. The waiting period for a pre-existing diseases cover is taken care of by the group cover.

Watch out for sub-limits

While supplementing an existing cover, you can either buy a normal policy or a topup plan. A top-up policy is cheaper because it will cover expenses beyond a certain initial threshold. For instance, Sharma, his wife and child already have a Rs 2 lakh health cover from their employers. They should ideally supplement this cover with a top-up policy. If they buy a normal cover of Rs 5 lakh, their premium will be at least Rs 10,000 per year. However, if they buy a top-up cover of Rs 5 lakh with a Rs 2 lakh deductible, it will cost them only Rs 4,100 a year, a saving of Rs 5,900 per year. Their existing policies can take care of the initial Rs 2 lakh, which won�t be covered by the top-up plan. Let us look at some other situations.

Self-employed or businessperson

Health insurance is especially important for people not in formal employment. For them, a simple indemnity plan that covers hospitalisation expenses will not be enough. They also need to insure themselves against loss of income due to hospitalisation. Most salaried people get paid medical leave, but if your company does not offer this benefit, a fixed benefit plan comes to the rescue. Self-employed professionals should supplement the base cover with a fixed benefit policy, which pays them a certain amount for the period that they are out of action.

Living with dependent parents

The family floater plan is not a good option if you want a cover for an older relative as well. This is because the premium rates in these plans are determined by the age of the oldest member. If you live with aged parents, it is advisable to go for individual policies rather than a family floater. Buy individual plans for them so that the premium for the rest of the family does not shoot up. Also, there is a greater likelihood of making a claim for an older person. So the floater plan will miss out on the no-claim bonus it might have otherwise received. |

|

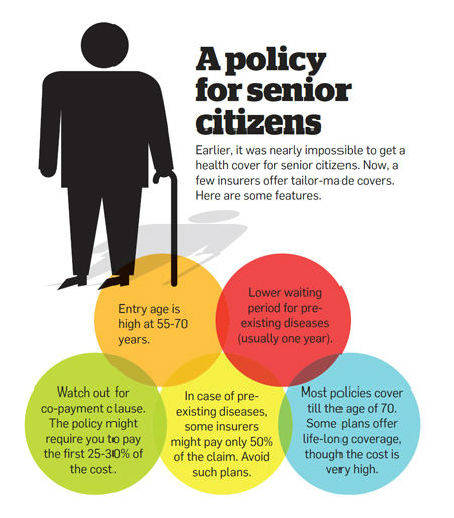

A policy for senior citizens

While buying a policy for your parents, study its features in great detail. Most health insurance policies don�t offer coverage beyond the age of 70 years, but some policies now offer a lifelong cover. "If the cover ceases at the age of 70, no other insurer will provide you one at that age. Opt for a policy that provides a life-long cover," advises Pankaj Mathpal, managing director of Optima Money Managers. However, do the math when you buy a health cover for someone over 70 years. The premium is prohibitively high and you could be paying Rs 24,000-30,000 a year for a cover of Rs 1.5 lakh. Some may find that putting away the premium money in an emergency fund for medical expenses is a better idea than buying insurance at that age.

If you still want to buy the cover, check out the clauses relating to renewability. Irda guidelines state that an insurer is bound to renew a policy except in case of evidence of fraud, moral hazard or misrepresentation. An insurer cannot back out because of the advancing age of the insured person. Insurers are also required to disclose upfront the terms of renewal, including the scope of coverage and the likely premium for future renewals. Swapan Khanna, co-founder of insurance tracking firm i-Save, says renewability should be among the most important factors governing the choice of a health policy. Look for disclosures regarding renewal of premiums� are they guaranteed on the basis of age slabs? According to the latest Irda guidelines, insurers cannot raise the premiums (called loading) arbitrarily on the basis of a claim in the previous year. It has to be based on the claims in the preceding three years. Besides, the company not only has to inform the policyholder of the rise three months in advance but also justify the increase.

Choosing the right policy

While choosing a policy, don�t be guided just by the premium being charged. The policy�s features are more important. Almost all policy documents are available on the Internet today. Download brochures and read the terms and conditions of policies carefully before making a choice.

Sub-limits:

Many policies come with sublimits on the sum assured. Besides room rent, there are sub-limits on surgeries, ICU charges and other procedures. The policies without sub-limits are better but charge higher premiums.

Co-payment:

Depending on how you look at it, this can be a boon as well as a bane. Copayment means the policyholder will bear a specified percentage of the claim amount, while the insurance company will foot the rest of the bill. This brings down the overall cost of insurance but also means you don�t get full coverage. There are various co-payment plans, including those that apply above a certain age or kick in when treatment is undertaken in a non-network hospital. The co-payment clause applies to plans that have differential premiums for metros and nonmetros. If you paid the lower premium applicable to a non-metro but get treated in a metro, the insurer may ask you to pay a part of the cost.

Network of hospitals:

Check if the hospitals you would prefer to go to are on the insurer�s network. Unless these hospitals are in the network, the cashless facility will not be available. A company may have 3,000 hospitals in its network and another may have only 2,000. Opt for the insurer which has tie-ups with reputed hospitals that you would prefer to go to. It�s even better if these hospitals are close to your house.

Exclusions:

Different health plans have different rules regarding exclusions. These are diseases and procedures that a policy will not cover, either for a specified time period or for the entire term. For instance, cataract or knee replacement may not be compensated for in the first two years. Insurers apply this rule to avoid having to pay in cases where people buy insurance covers after they have been diagnosed with a disease. Stay away from policies that have too many exclusions or where the cooling-off period is very long.

Day-care procedures:

Many policies do not compensate you unless you are hospitalised for at least 24 hours. Day-care procedures are normally not covered. However, nowadays, owing to improvements in technology, you don�t need to get hospitalised for several procedures, including non-invasive or laparoscopic surgeries. Some of the newer policies recognise this fact. Opt for plans that cover the maximum number of day-care procedures.

Alternative treatments:

Some policies also cover alternative treatments such as homoeopathic, Unani and ayurvedic medicine. But such alternative methods are highly recommended for the treatment of some diseases. It is better to opt for policies that also cover such alternative treatments, though these will cost more than the normal plan that covers only allopathic treatment. To make your task of choosing a policy easier, we have provided ratings of health insurance policies, which you can consult.

How to counter rise in costs

Case of Yashpal Raulji

Health insurance premiums are set to go up soon. PSU insurer New India Assurance Company has already received Irda�s nod for hiking the premium by 20%, and others are likely to follow suit. "With a one-time market adjustment of 10-20% proposed by PSU insurers, health insurance premiums may increase further this year," says Anuradha Sriram, benefits director, Tower Watson India. One contributory factor is the fragmented and unorganised nature of India�s healthcare industry. If it was well-organised, diagnostic procedures and treatment protocols could be standardised and there would be uniform pricing. "Since examination and treatment costs are not standardised, there is limited scope for controlling costs. Healthcare providers often engage in excessive treatment and then overcharge, which results in higher bills," says Khanna of i-Save. Insurers also have to bear the burden of the administrative costs involved in dealing with a vast network of healthcare providers.

The pharma industry chips in with high R&D costs and expensive drugs. Once a new molecule has been created and successfully clears several rounds of clinical trials, the drug manufacturer gets a patent for a limited number of years. It is during this period that the manufacturer tries to recover the R&D cost and make a profit. When the period ends, competition from generics comes in. Hence, prices of new drugs tend to be high. India has the Drug Price Control Order (DPCO), under which prices of several drugs are capped. Says Vishal Dhawan, chief financial planner at Mumbai-based Plan Ahead Wealth Advisors: "While the DPCO is meant to benefit end-users, it has ended up creating a set of distortions in the market." A company that sells both types of drugs�those that come under DPCO and those that don�t�often tries to maximise its profits by pricing its non-DPCO drugs higher.

There is not much you can do to shield yourself from the rising cost of insurance. However, you can control costs by making smart choices. Some financial planners suggest that besides health insurance, you should also set aside a corpus for medical emergencies. This option may not always be feasible, but an increasing number of people is opting for it. Their reasoning: if there is an emergency and your policy can�t cover the full expense, you have something handy to ensure the best healthcare available. "If you don�t suffer from any health problem, the money still stays with you," says Mathpal.

Sriram says that a better way of keeping costs down is to adopt preventive healthcare measures. In other words, live a healthy lifestyle and exercise regularly. The bottom line, however, is that in this age of rising healthcare costs you need to protect your family by buying adequate insurance and spending your money on the right policy.